The bring-forward rule is automatically triggered as soon as you make a non-concessional contribution that exceeds the annual cap. For example, if you contributed $150,000 as a non-concessional contribution in the 2020–2021 financial year, this would be $50,000 over the annual cap.

Can you bring-forward concessional contributions?

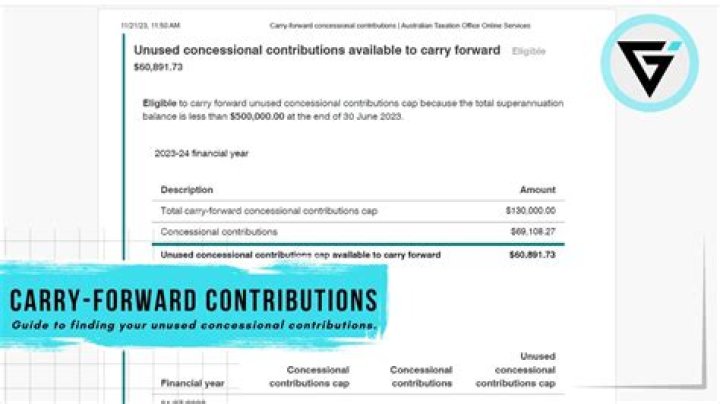

Unused concessional cap carry forward From 1 July 2018, members can make ‘carry-forward’ concessional super contributions if they have a total superannuation balance of less than $500,000. Members can access their unused concessional contributions caps on a rolling basis for five years.

What does non-concessional contribution mean?

Non-concessional contributions (NCCs) are super contributions made from after-tax pay or savings. They include: personal contributions you make into your own super account that are not claimed as a tax deduction. personal contributions made by your spouse into your super account (spouse contributions), and.

Is it worth making non-concessional contributions?

Making non-concessional contributions to your spouse’s super fund can be an effective strategy to reduce, or even eliminate, the amount of tax you pay. This strategy can also assist in equalising the level of retirement savings that you and your spouse have.

What are carry forward contributions?

Broadly, the carry forward rule allows individuals to make additional CC in a financial year by utilising unused CC cap amounts from up to five previous financial years, providing their total superannuation balance just before the start of that financial year was less than $500,000.

What is concessional contribution?

Concessional contributions are contributions that are made into your super fund before tax. They are taxed at a rate of 15% in your super fund.

What are concessional and non concessional contributions?

Concessional contributions are contributions made by your employer or that you make with ‘before-tax’ dollars, like salary sacrificing. Non-concessional contributions include spouse contributions and contributions you make from ‘after-tax’ dollars.

Can I make non concessional contributions?

If you are a member of a self-managed superannuation fund (SMSF) you may be able to make a non-concessional contribution in one financial year and have it count towards your non-concessional contributions cap in the following financial year.

What is the difference between concessional and non concessional contributions?

Which is better concessional or non-concessional contributions?

The non-concessional contribution cap of $100,000 per financial year is four-times higher than the concessional contribution cap of $25,000 per year. Allowing you to get more into super. While under age 65, an individual is able to ‘bring-forward’ up to two years of the non-concessional contribution cap.

Can I claim non-concessional contributions?

Need to know: You cannot claim a tax deduction for personal contributions you want to keep as non-concessional (after-tax) contributions.

What is bring forward non-concessional?

Bring-Forward Non-Concessional Contributions The Bring-forward rule is a provision that allows Members to make non-concessional contributions (after-tax contributions) amounting to more than the contributions cap of $100,000 over a three-year period.

What is the cap on non-concessional contributions?

For NCCs, the cap is currently set at $100,000. This is four times the annual concessional (before-tax) contribution cap. Under the ‘bring-forward’ arrangement, members who are under 67 at any time in the financial year may effectively bring-forward up to two years’ worth of non-concessional caps.

Can I make a non-concessional contribution to my SMSF?

If you are a member of a self-managed superannuation fund (SMSF) you may be able to make a non-concessional contribution in one financial year and have it count towards your non-concessional contributions cap in the following financial year. You and your SMSF will need to meet several conditions.

Can I make non-concessional contributions if I am under 65?

If you are under 65 years of age at any time in a financial year, you may be able to make non-concessional contributions of up to three times the annual non-concessional contributions cap in that financial year. If you are 65 years old or older on 1 July, you cannot access the bring-forward arrangement in that financial year.