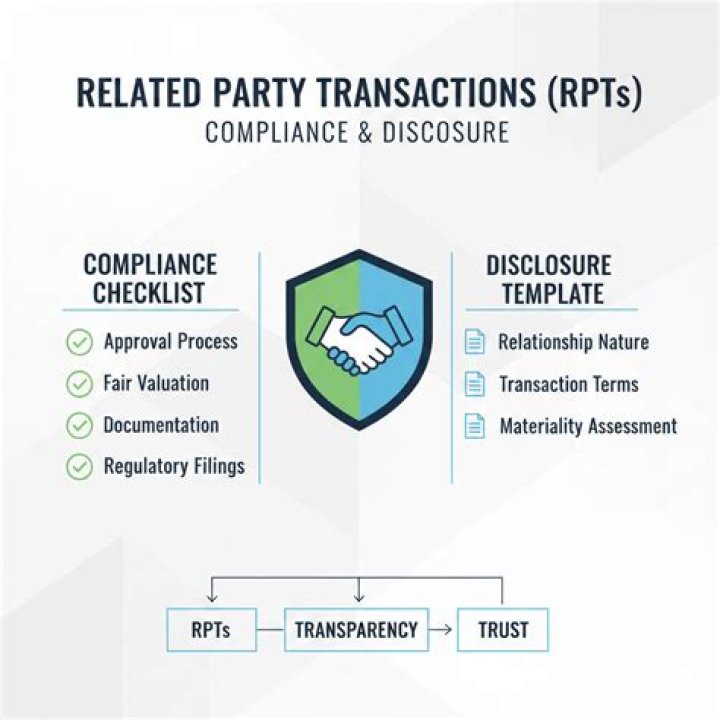

IAS 24 has no special recognition or measurement requirements for related party transactions. However, it requires companies to disclose transactions and outstanding balances, including any commitments, with related parties.

What do you disclose in related party transactions?

If the entity has transactions with the related party during the financial year, then it shall disclose the nature of such transactions, and also all the details such as amount, outstanding balances including commitments, provision for doubtful debts, and the expense recognised in respect of bad and doubtful debts.

What are related party disclosures what should be disclosed?

IAS 27 — Consolidated and Separate Financial Statements (2008) IAS 28 — Investments in Associates and Joint Ventures (2011) IAS 28 — Investments in Associates (2003) IAS 29 — Financial Reporting in Hyperinflationary Economies. IAS 30 — Disclosures in the Financial Statements of Banks and Similar Financial Institutions.

What are the minimum disclosures for related party transactions?

What needs to be disclosed under AS 18

- The name of the transacting related party;

- A description of the relationship between the parties;

- A description of the nature of transactions;

- Volume of the transactions either as an amount or a part thereof;

Is directors remuneration a related party transaction?

Remuneration paid to key management personnel should be considered as a related party transaction requiring disclosures under AS 18. In case non-executive directors on the Board of Directors are not related parties, remuneration paid to them should not be considered a related party transaction.

What is the purpose of related party transactions?

A related-party transaction is an arrangement between two parties that have a preexisting business relationship. Some, but not all, related party-transactions carry the innate potential for conflicts of interest, so regulatory agencies scrutinize them carefully.

Are directors considered related parties?

In the author’s view, there is no requirement of treating Director’s remuneration as a RPT as long as the sum of money paid to the director is the ‘remuneration to which he is entitled as director’. The definition of related party clearly indicates that every director is considered to be a related party to the Company.

Is director a related party?

Is director remuneration a related party transaction?

Are directors of a company related parties?

As per the definition of related party, a Director of a company or his/her relative is also a related party to the company.

What is considered a related party transaction?

A related-party transaction is a business deal or arrangement between two parties who are joined by a preexisting special relationship.

What are related party disclosures?

Purpose of related party disclosures. The objective of IAS 24 is to ensure that financial statements contain the disclosures necessary to draw attention to the possibility that the reported financial position and results may have been affected by the existence of related parties and by transactions and outstanding balances with related parties.

What is the definition of related party transactions?

related party transactions. A business deal, transaction, or conveyance among parties that have a special relationship with each other, either through family ties, related corporations, or other possibilities.

What is related party disclosure?

The disclosure of related party information is considered useful to the readers of a company’s financial statements, particularly in regard to the examination of changes in the financial results and financial position over time, and in comparison to the same information for other businesses. Examples of related parties are: