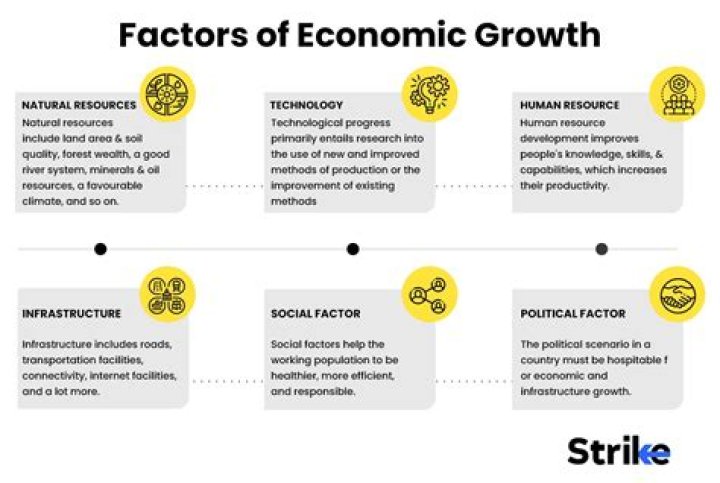

In economics, it is widely accepted that technology is the key driver of economic growth of countries, regions and cities. Technological progress allows for the more efficient production of more and better goods and services, which is what prosperity depends on.

How does technology improve productivity and economic growth?

The study found out that growth in technological progress resulted in economic growth, whereas increase in either capital productivity or labor productivity gave rise to reduction in economic growth within the aforementioned period.

What is the most important contributor to economic growth?

First, technology is typically the most important contributor to U.S. economic growth. Growth in human capital and physical capital often explains only half or less than half of the economic growth that occurs.

What is the relationship between productivity and technology?

Increases in total factor productivity reflect a more efficient use of inputs, and total factor productivity is often taken as a measure of long-term technological change or dynamism brought about by such factors as technical innovation.

Technological development brings economic growth. Causing increased communication, easy and fast access to the new markets, increase in the marketing channels and company mergers, technological development made a positive impact to the economy.

How does technology contribute to development?

The rapid spread of technology fueled by the Internet has led to positive cultural changes in developing countries. Easier, faster communication has contributed to the rise of democracy, as well as the alleviation of poverty. Globalization can also increase cultural awareness and promote diversity.

How does technology affect the economic system?

Technology has deeply affected the global economy and its usage has been linked to marketplace transformation, improved living standards and more robust international trade. Technological advances have significantly improved operations and lowered the cost of doing business.

How does technology can enhance economic growth and innovation?

Technology fosters innovation, creates jobs, and boost long-term economic prosperity. By improving communication and creating opportunities for data-sharing and collaboration, information technology represents an infrastructure issue as important as bridges, highways, dams, and buildings.

What is the role of science and technology in development?

Science and Technology hold the key to the progress and development of any nation. Technology plays a Fundamental role in wealth creation, improvement of the quality of life and real economic growth and transformation in any society.

How are technology and economic growth related to each other?

The technology can be regarded as primary source in economic development and the various technological changes contribute significantly in the development of underdeveloped countries. Technological advancement and economic growth are truly related to each other. The level of technology is also an important determinant of economic growth.

How does information technology affect the US economy?

Here are the five common economic effects of ICT. The ICT sector is, and is expected to remain, one of the largest employers. In the US alone, computer and information technology jobs are expected to grow by 22% up to 2020, creating 758,800 new jobs.

Why is technological progress important to the economy?

Now, the importance of technological progress is that it can suspend the occurrence of stationary state equilibrium. Classical economists underestimated the role of technological progress in preventing the occurrence of stationary state equilibrium. When technical progress occurs it will raise the productivity of capital and labour.

How is rapid rate of growth achieved through technology?

The rapid rate of growth can be achieved through high level of technology. Schumpeter observed that innovation or technological progress is the only determinant of economic progress. But if the level of technology becomes constant the process of growth stops. Thus, it is the technological progress which keeps the economy moving.