Adjustment in Profit and Loss account – Prepayments Adjustments are made in Final accounts to show the true view of their transactions. They are closing entries or amendments made in the books at the end of the of accounting period in order to match revenue with expenses.

How do you prepare a trading profit and loss account in accounting?

How do you calculate the profit or loss?

- Add all the income earned during the accounting period.

- Add all the expenses incurred during the accounting period.

- Calculate the difference by subtracting total expenses from total income.

- If the value is positive then it is profit, if negative it is loss.

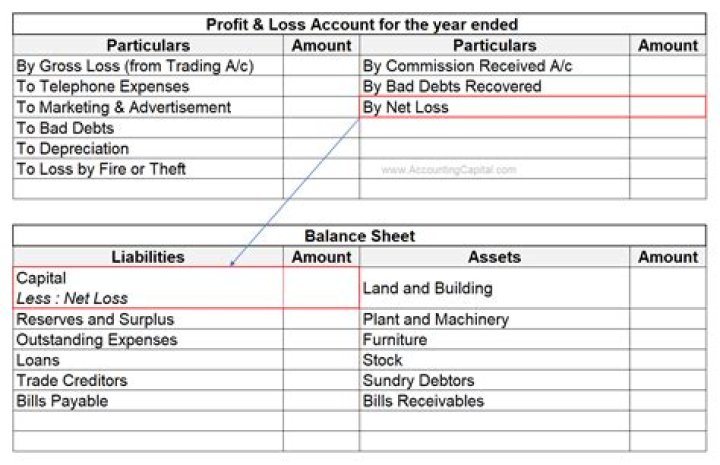

How do you do trading profit and loss account and balance sheet?

In order to arrive at the balance sheet of a business, one needs to prepare the trading account and profit and loss account first. This account is prepared to arrive at the figure of revenue earned or loss incurred during a period. Let us understand the trading account and profit and loss account in detail.

What comes under trading and profit and loss account?

The trading account gives information related to profit earned or loss through various trading activities. Whereas the profit and loss, account determine the net profit or loss for the period. Trading and P&l accounts are used to calculate the gross profit and net profit of the organization.

How do you adjust a profit and loss account?

Balance the profit and loss report. Add a line at the bottom of the report labeled “Net Income.” Subtract the total expenses from the total revenue. Enter this total as the net income figure. Update the date at the top of the report to reflect the period that the adjusted balance applies to.

What are the 5 types of adjusting entries?

Adjustments entries fall under five categories: accrued revenues, accrued expenses, unearned revenues, prepaid expenses, and depreciation.

What is profit and loss account with example?

A profit and loss account shows a company’s revenue and expenses over a particular period of time, typically either one month or consolidated months over a year. The profit and loss account represents the profitability of a business. It cannot, for example, show you if you are running out of cash as you build stock.

What is trade account give an example?

All direct expenses like Carriage inward & Freight expenses, Rent for godown or factory, Electricity and Power expenses, wages of workers and supervisors, Packing expenses, etc.

How do you calculate adjusted profit?

Adjusted Profit So if you have revenue of $200,000 and $150,000 in expenses that include $60,000 in salary and other benefits for the owner, your adjusted net profit margin is $110,000 divided by $200,000, or 55 percent.

What are the four types of adjustments?

There are four specific types of adjustments:

- Accrued expenses.

- Accrued revenues.

- Deferred expenses.

- Deferred revenues.

What is AP and L statement?

A P and L statement, also known as a profit and loss statement, is a financial report that summarizes revenue, costs, and expenses incurred over a fiscal quarter or year. This report is especially useful as it shows a business’s financial health and profitability.

What is the purpose of trading and profit and loss?

Trading and profit and loss accounts are useful in identifying the gross profit and net profits that a business earns. The motive of preparing a trading and profit and loss account is to determine the revenue earned or the losses incurred during the accounting period. How do you calculate gross profit in a trading account?

What is another name for profit and loss account?

Another name given to a trading profit and loss account is the income statement. How do you calculate the profit or loss? To determine accounting profit and loss perform the following steps Add all the income earned during the accounting period.

What is the difference between tradtrading and profit and loss account?

Trading and Profit and Loss Account format is represented separately as follows: Trading Account is prepared first and then profit and loss account is prepared. Profit/Loss Account is prepared after the trading account is prepared. It is the first stage in the creation of the final account.

How to avoid overstating profits adjustments in final accounts?

In order to avoid overstating profits adjustments in final accounts are recorded. Examples: Outstanding Rent, Salary, Wages, Interest, etc. Suppose a company paid Rs 10,000 in salaries during the year and evaluates outstanding salaries at Rs 2,000 at the end, show the adjustment of outstanding expense in final accounts.