A principle is feasible to the extent that it can be implemented without much complexity or cost. These criteria often conflict with each other, e.g., information about the value of a new product to the inventor is indeed relevant.

What is the meaning of consistency principle in accounting?

The consistency principle states that, once you adopt an accounting principle or method, continue to follow it consistently in future accounting periods so that the results reported from period to period are comparable. This was disclosed, as required by GAAP, in the footnotes to the audited financial statements.

What is capital principle in accounting?

(A-L=C) It is the claim of the owners on assets. Capital or Owners Equity is simply called capital or if the business is a corporation it is called Capital Stock. There is an account that reduces capital. When the owners take something out of the business they have a withdrawal or drawing.

What is GAAP principle in accounting?

Generally Accepted Accounting Principles (GAAP or US GAAP) are a collection of commonly-followed accounting rules and standards for financial reporting. The purpose of GAAP is to ensure that financial reporting is transparent and consistent from one organization to another.

What is a consistency principle?

What is the Consistency Principle? The consistency principle states that, once you adopt an accounting principle or method, continue to follow it consistently in future accounting periods. Only change an accounting principle or method if the new version in some way improves reported financial results.

What is consistency principle example?

Example of the consistency principle: Company A’s Financial Statements report base on IFRS. Its accounting policies for depreciation are using a straight-line basis. All of the change requires full disclosure in the financial statements and how the change affected. This is how we apply the Consistency Principle.

What are the 3 basic accounting principles?

Take a look at the three main rules of accounting: Debit the receiver and credit the giver….

- Debit the receiver and credit the giver.

- Debit what comes in and credit what goes out.

- Debit expenses and losses, credit income and gains.

What are the 5 principles of accounting?

5 principles of accounting are;

- Revenue Recognition Principle,

- Historical Cost Principle,

- Matching Principle,

- Full Disclosure Principle, and.

- Objectivity Principle.

What is GAAP and non GAAP?

GAAP stands for Generally Accepted Accounting Principles, lays down a uniform set of rules and formats, along with guidelines for measurement, presentation, disclosure and recognition where companies need to follow in its method of accounting, on the other hand, Non-GAAP is any method of accounting followed by the …

What is IFRS and GAAP?

An Overview of GAAP vs. IFRS. GAAP, also referred to as US GAAP, is an acronym for Generally Accepted Accounting Principles. This set of guidelines is set by the Financial Accounting Standards Board (FASB) and adhered to by most US companies. IFRS stands for International Financial Reporting Standards.

What is the realization principle in accounting?

The realization principle is the concept that revenue can only be recognized once the underlying goods or services associated with the revenue have been delivered or rendered, respectively. Thus, revenue can only be recognized after it has been earned. The best way to understand the realization principle is through the following examples:

What are the accounting principles of the US?

The common set of U.S. accounting principles is the generally accepted accounting principles (GAAP). To remain listed on many major stock exchanges in the U.S., companies must regularly file financial statements reported according to GAAP.

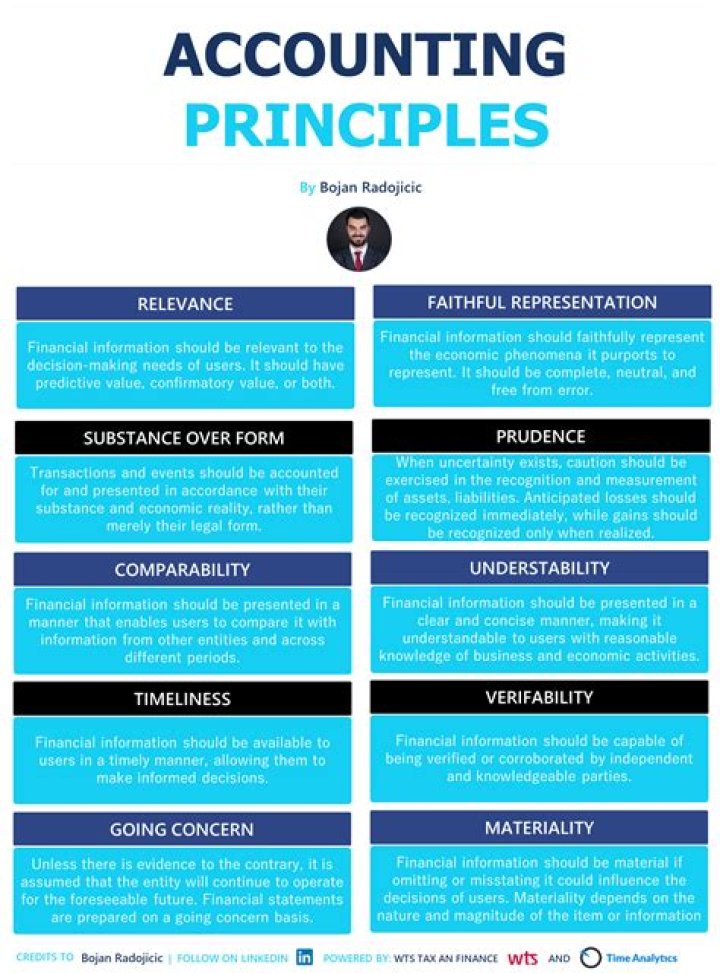

Why is the materiality principle important in accounting?

The materiality principle is especially important when deciding whether a transaction should be recorded as part of the closing process, since eliminating some transactions can significantly reduce the amount of time required to issue financial statements.

When accounting principles allow a choice between multiple accounting methods?

When accounting principles allow a choice between multiple methods, a company should apply the same accounting method over time or disclose its change in accounting method in the footnotes to the financial statements .