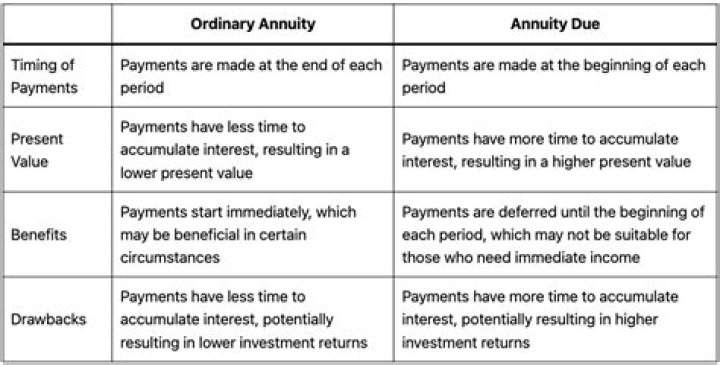

An ordinary annuity means you are paid at the end of your covered term; an annuity due pays you at the beginning of a covered term.

What is present value annuity due?

The present value of an annuity due (PVAD) is calculating the value at the end of the number of periods given, using the current value of money. Another way to think of it is how much an annuity due would be worth when payments are complete in the future, brought to the present.

What do you mean by ordinary annuity and annuity due?

An ordinary annuity is a series of regular payments made at the end of each period, such as monthly or quarterly. In an annuity due, by contrast, payments are made at the beginning of each period. Consistent quarterly stock dividends are one example of an ordinary annuity; monthly rent is an example of an annuity due.

Why does annuity due earns more?

Conversely, an annuity due is most advantageous for a consumer when they are collecting payments. The payments made on an annuity due have a higher present value than an ordinary annuity due to inflation and the time value of money.

What is an example of annuity?

An annuity is a series of payments made at equal intervals. Examples of annuities are regular deposits to a savings account, monthly home mortgage payments, monthly insurance payments and pension payments. The payments (deposits) may be made weekly, monthly, quarterly, yearly, or at any other regular interval of time.

Which is more valuable ordinary annuity or annuity due?

Since payments are made sooner with an annuity due than with an ordinary annuity, an annuity due typically has a higher present value than an ordinary annuity. On the other hand, when interest rates fall, the value of an ordinary annuity goes up.

What is the difference between annuity due and perpetuity?

When calculating the time value of money, the difference between an annuity derivation and perpetuity derivation is related to their distinct time periods. An annuity is a set payment received for a set period of time. Perpetuities are set payments received forever—or into perpetuity.

Why would you prefer to receive an annuity due for $10000 per year for 10 years than an otherwise similar ordinary annuity?

Why would you prefer to receive an annuity due for $10,000 per year for 10 years than an otherwise similar ordinary annuity? Because each payment occurs one period earlier with an annuity due, all of the payments earn interest for one additional period.

What are some examples of annuities?

Examples of annuities are regular deposits to a savings account, monthly home mortgage payments, monthly insurance payments and pension payments. Annuities can be classified by the frequency of payment dates.

How do you calculate the present value of an annuity due?

The formula for calculating the present value of an annuity due (where payments occur at the beginning of a period) is: P = (PMT [(1 – (1 / (1 + r)n)) / r]) x (1+r) Where: P = The present value of the annuity stream to be paid in the future. PMT = The amount of each annuity payment. r = The interest rate.

What is the difference between an annuity due vs. an ordinary annuity?

The points given below are noteworthy, so far as the difference between ordinary annuity and annuity due is concerned: Ordinary annuity refers to the sequence of steady cash flow, whose payment is to be made or received at the end of each period. Each cash inflow or outflow of an ordinary annuity is related to the period preceding its date.

What are the disadvantages of annuity?

The main disadvantage of Annuities is that your money is not 100% liquid until your term is over. Some annuities have more liquidity than others; most offer 10% yearly penalty free liquidity. Some offer up to 20% yearly liquidity, while some just offer 5%.

What is an annuity and how does it work?

In its simplest form, an annuity is an agreement in which you make one or multiple payments in exchange for receiving a set amount of income for a period of time. They’ve been around for a long time and are commonly used by conservative retirees who want to make sure that they’ll have a regular income for the rest of their lives.